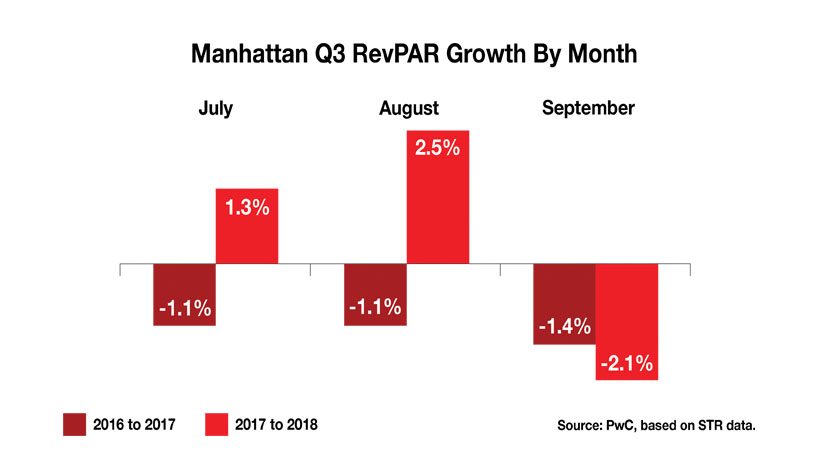

NEW YORK—Growth in average daily room rate (ADR) began to slow from the first half of 2018, minimizing gains in revenue per available room (RevPAR) for Manhattan hotels, according to the quarter 2018 edition of the PwC Manhattan Lodging Index.

During the third quarter, minimal increases in lodging supply exceeded growth in demand, with occupancy posting declines year-over-year. As pricing power diminished over the summer months for the Manhattan lodging market, RevPAR remained relatively flat over prior year levels, increasing 0.2%.

ADR growth fell 3.3% from the prior quarter, as price-sensitive leisure guests replaced the business traveler over the summer months, but increased 0.8% over the prior year. Despite stymied growth across key metrics during the quarter, Q3 2018 occupancy of 90.4% contributed to the highest year-to-date occupancy level for Manhattan hotels over the 24-year period tracked.

For luxury hotels, occupancy levels were down from the prior year at 83.4%, while ADR held strong, increasing 3% percent from Q3 2017 levels. Upper-upscale hotels, which posted the only declines in ADR across all Manhattan hotel classes, reported a 1.5% decrease in RevPAR, equally driven by a 0.8% decline in occupancy and 0.7% decrease in ADR. For hotels categorized as upscale and upper-midscale, RevPAR grew at 1% and 1.3%, respectively. ADR growth of 1.1% and 1.6%, respectively, was partially offset by slight declines in occupancy over prior year levels.

All Manhattan submarkets, with the exception of Upper Manhattan and Midtown West, posted increases in RevPAR during the third quarter. Midtown East, which experienced the largest RevPAR growth of 3.6%, also posted the largest increase in ADR at 4.3%. Lower Manhattan, which saw growth in RevPAR of 1.4%, experienced gains from ADR increases, despite a decline in occupancy of 0.5%. For Midtown South, where occupancy fell by 1% during the quarter, ADR-driven RevPAR growth of 0.3% resulted from an increase in ADR of 1.4%. Midtown West, which fell victim to both declines in occupancy and ADR of 0.4% and 0.6%, respectively, experienced a decline in RevPAR of 1% over the prior year.

Of the five Manhattan submarkets tracked, Upper Manhattan experienced the largest decline in occupancy year-over-year, despite room supply remaining flat during the same period. Posting the largest decline in RevPAR for the quarter, Upper Manhattan’s 2.3% decrease was driven by occupancy declines of 4.2%, partially offset by an increase in ADR of 1.9%. Growth in RevPAR for limited-service hotels was slightly higher than that of full-service hotels during Q3. Despite decreases in occupancy for limited-service hotels exceeding that of full-service hotels, ADR-driven RevPAR growth resulted from increases in ADR of 1.5% and 0.8%, respectively. In Manhattan, chain-affiliated hotels continued to lag independent hotels in terms of ADR growth during the third quarter. While occupancy fell for both by 0.4% and 1.1%, respectively, ADR increased by 0.1% and 1.9%, respectively.